AI in Healthcare: Top USA Startups Leading the Future

The healthcare industry is standing on the brink of a massive transformation, and at the heart of this revolution is Artificial Intelligence (AI). From predicting diseases before they occur to assisting surgeons with robotic precision, AI is no longer a sci-fi dream—it’s a medical reality. In 2026, USA-based startups are spearheading this change, pushing the boundaries of what’s possible in patient care and diagnostics. In this guide, we will explore how these innovative startups are leading the global healthcare landscape and why their solutions are essential for the future of medicine.

AI in Healthcare: How USA Startups are Leading — the rapid rise of AI-driven startups is reshaping US healthcare delivery and research. You’ll see how companies like Tempus, Olive AI, PathAI, Insitro, and Viz.ai are turning machine‑learning models into diagnostic tools, workflow automations, and precision‑medicine platforms that hospitals and labs adopt quickly.

💡

Did You Know?

US AI healthcare startups like Tempus, Olive AI, PathAI, Insitro, and Viz.ai have rapidly scaled clinical tools and research platforms, drawing major venture interest and accelerating adoption across hospitals and labs.

Source: Industry reports & company press releases

This review helps you navigate the landscape and funding trends, assesses top use cases and clinical impact, compares startups and technologies, weighs pros and cons, and delivers practical takeaways you can apply as an investor, clinician, or product leader.

- Landscape & funding trends

- Key clinical use cases

- Startup comparisons & outcomes

- Business models, regulation, and adoption

- Balanced pros and cons

Why USA Startups Lead in AI Healthcare

Why US Startups Win

▶

Concentration of Talent

Clusters at MIT, Stanford, Johns Hopkins, and teams from Google Health and Microsoft Research feed startups like PathAI and Caption Health.

▶

Capital & VC Appetite

Venture firms (Sequoia, Andreessen Horowitz) and corporate funds fuel trials and scaling for Tempus and Flatiron Health.

▶

Access to Clinical Data

Partnerships with Mayo Clinic, Kaiser Permanente, and UCSF enable real-world datasets for Freenome and Viz.ai.

▶

Regulatory Pathways

FDA programs (Breakthrough Device, 510(k), De Novo) and commercialization support accelerate products like Olive AI.

▶

Accelerators & Ecosystem

Y Combinator, JLABS, and MassChallenge provide mentorship, plus interdisciplinary talent crossing biomedicine and ML.

Drivers

You see US startups lead because of tightly linked talent hubs and clinical centers. Top universities like MIT, Stanford, and Johns Hopkins, together with big tech labs at Google Health and Microsoft Research, supply interdisciplinary teams that power PathAI, Caption Health, and Tempus.

Venture capital is another force; Sequoia and Andreessen Horowitz, corporate funds, and strategic investors accelerate clinical trials and commercialization for companies such as Flatiron Health and Freenome.

Access to large, real‑world datasets through partnerships with Mayo Clinic, Kaiser Permanente, and UCSF gives models statistical power and speeds validation for tools like Viz.ai and Olive AI.

Regulatory pathways, including FDA Breakthrough Device, 510(k), and De Novo routes, create pragmatic commercialization paths, while accelerators such as Y Combinator and JLABS provide mentorship and pilot access.

You should weigh ecosystem strength against competition; the same dynamics that enable rapid iteration attract acquisitions and aggressive scaling, exemplified by Flatiron’s Roche deal and Broad’s interest in diagnostics startups.

The startup culture favors product‑market fit and iterative clinical deployment. Teams at companies like Caption Health iterate ultrasound models in real clinics, while Tempus combines genomic pipelines and clinical workflows to shorten time to actionable insights.

Interdisciplinary talent—clinician‑engineers, data scientists, regulatory experts—paired with accelerator programs like MassChallenge and strategic partnerships with health systems, ensure you can pilot, measure, and scale with rigor.

If you follow AI in Healthcare: How USA Startups are Leading, note that this concentrated ecosystem reduces time from prototype to trial, but you must scrutinize data bias, reproducibility, and clinical utility for any vendor. This balance drives investment and outcomes.

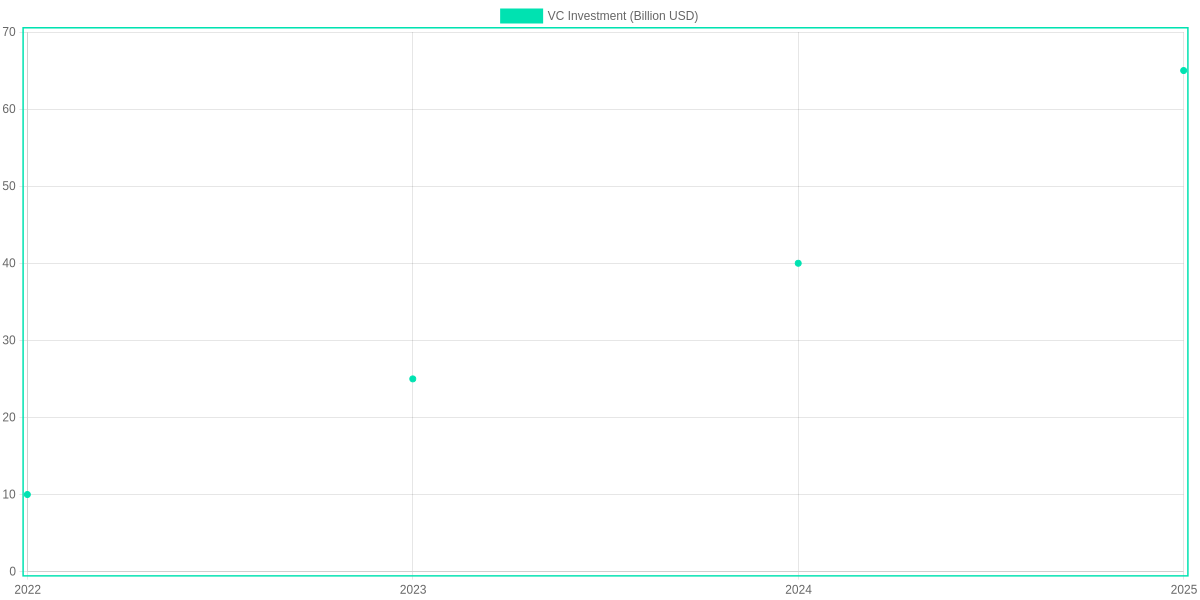

Market Landscape & Funding Trends

The global AI in healthcare market is projected at roughly $45B by 2026, with the United States accounting for an estimated 30–40% share — roughly $13.5–$18B. That concentration reflects strong clinical data pipelines, regulatory focus, and large payer/provider markets that favor rapid scaling.

Investor behavior and priorities

VCs have increased allocations to AI-health startups, illustrated by steep multi-year growth in disclosed rounds and crossover financing. Investors prioritize solutions that show near-term reimbursement paths and strong clinical validation, which helps explain why diagnostics, workflow automation, drug discovery, and remote monitoring dominate deal activity.

Funding Focus Areas

US investors are concentrating on diagnostics, workflow automation, drug discovery, and remote monitoring — driving product launches and partnerships.

- ✓ Diagnostics (imaging & pathology)

- ✓ Workflow automation (Olive, Caption Health)

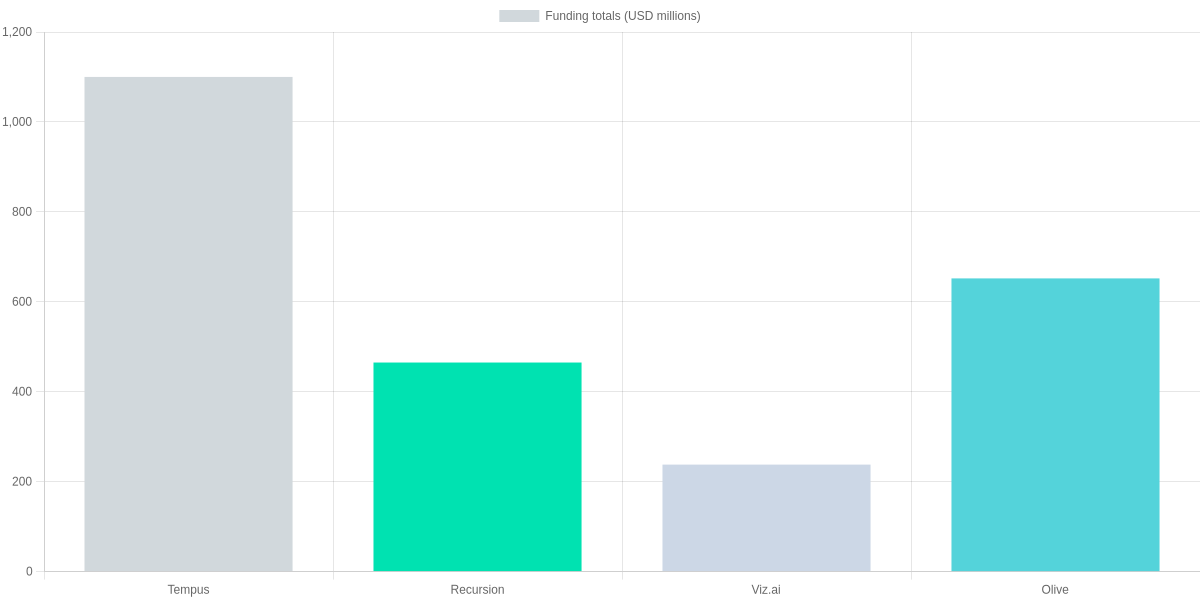

- ✓ Drug discovery (Tempus, Recursion)

- ✓ Remote monitoring (AliveCor, Biofourmis)

M&A, exits, and what it means for you

Strategic deals and exits — Roche’s acquisition of Flatiron Health and high-profile public listings such as Butterfly Network — have accelerated consolidation and validated business models. Illumina’s attempted acquisition of GRAIL also signaled strong commercial interest in diagnostics.

- Roche — Flatiron Health (strategic acquisition)

- Butterfly Network — IPO (public market validation)

- Illumina — GRAIL (large strategic deal attempt)

For you this means faster access to FDA-cleared products, more partnership options with established platforms, and tougher competition when you evaluate vendors. Expect more integrations (EHR, imaging), broader commercial pilots, and a larger vendor pool to compare when selecting AI tools for clinical workflows.

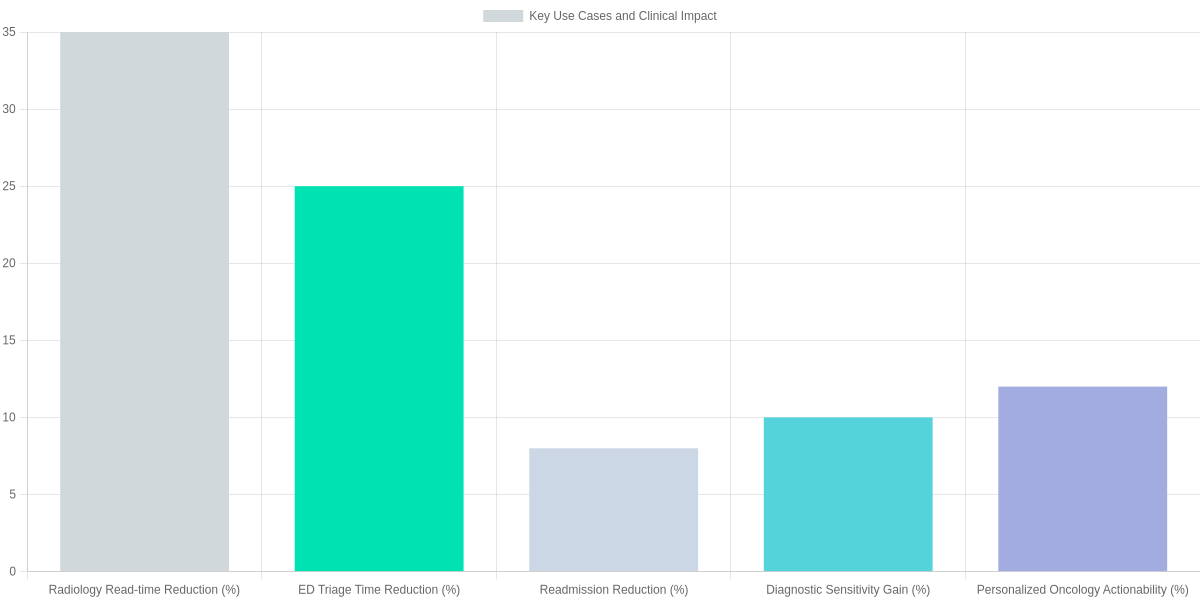

Key Use Cases and Clinical Impact

Radiology and image interpretation, digital pathology, ED triage/workflow, predictive analytics for readmissions, and personalized oncology are where U.S. startups are most active. Companies such as Aidoc and Viz.ai focus on imaging prioritization, PathAI targets histopathology, Qventus addresses ED flow, and Tempus pushes oncology decision support.

Top clinical applications

Radiology AI targets faster reads and prioritization; PathAI and similar tools aim to improve diagnostic sensitivity in histology. Predictive models flag patients at risk for 30‑day readmission, and oncology platforms increase identification of actionable biomarkers to guide therapy selection.

Implementation steps for clinical adoption

1️⃣

Choose the right use case

Match Aidoc or Viz.ai for radiology prioritization, PathAI for histopathology, and Tempus for oncology insights.

2️⃣

Validate locally

Run retrospective validation on your EHR and PACS; confirm radiology read-time and sensitivity gains.

3️⃣

Integrate into workflow

Embed Viz.ai/Aidoc alerts into PACS, connect Qventus to ED dashboards for real-time triage.

4️⃣

Monitor outcomes

Track metrics: read-time, readmission rates, diagnostic sensitivity, and treatment actionability.

5️⃣

Engage regulators & compliance

Confirm FDA clearance status and post-market surveillance plans; document local performance.

Impact metrics and evidence

Pilot and vendor-reported figures show radiology read‑time reductions commonly between 20–50% and diagnostic sensitivity gains that vary by condition. Readmission-focused pilots report single‑digit to low double‑digit percentage drops; the chart below visualizes representative impact sizes across domains. Regulators have cleared 500+ AI/ML‑enabled devices, underscoring rapid adoption but also the need for post‑market data.

Evidence gaps remain: peer‑reviewed outcomes are heterogeneous, and independent validation is often limited. You should validate models on your local data, watch for workflow friction and alert fatigue, and monitor outcomes continuously to ensure efficiency gains translate to better patient care.

Startup Comparisons: Companies, Technologies, and Outcomes

You need comparable benchmarks to evaluate AI vendors across diagnostic AI, workflow automation, drug discovery, and population-health platforms. Below I contrast representative US startups on core technology, clinical validation, FDA/regulatory standing, business model, funding scale, and reported pilot outcomes so you can prioritize what to request during vendor due diligence.

How to evaluate vendors (practical checklist)

Vendor Evaluation Steps

Assess Validation

Request sensitivity/specificity, study size, PPV/NPV, and peer-reviewed papers.

Confirm Regulatory Standing

Check 510(k)/De Novo/clearance or INDs; ask for FDA letters and CE markings.

Evaluate Interoperability

Ask for EHR integrations (Epic/Cerner), FHIR support, HL7 interfaces, and deployment time.

Review Business Terms

Clarify SaaS vs per-use pricing, licensing fees, and reimbursement pathways.

Verify Customer Evidence

Obtain reference sites, deployment case studies, and real-world performance data.

| Feature | Viz.ai | Olive | Recursion |

|---|---|---|---|

| Core technology | Deep learning for CT/LVO detection; CNNs | RPA + ML workflow orchestration; process automation | High-throughput phenomics + ML for drug discovery |

| Clinical validation level | Multiple peer-reviewed case series and multi-center deployments | Operational pilots; workflow ROI case studies | Preclinical screens and early translational studies; partnerships with pharma |

| Regulatory / FDA status | FDA-cleared for LVO triage (stroke) | Not an FDA medical device (enterprise automation) | Not a device; INDs and clinical programs in progress |

| Business model | SaaS/per-use imaging alerting with hospital contracts | SaaS/licensing for automation with per-transaction pricing | Partnership/licensing with pharma; internal drug pipeline investments |

| Reported outcomes | Reported 30–40% faster time-to-treatment in pilots | Reported 30–60% reduction in manual processing time in ops pilots | Reported 5–10x hit discovery throughput in preclinical screens |

Quick pros & cons (review lens)

- Pros: Companies like Viz.ai demonstrate clear clinical endpoints (reduced time-to-treatment); drug-discovery firms (Recursion) scale hit-finding throughput; workflow vendors (Olive) yield measurable admin savings.

- Cons: Varying validation rigor (many pilots vs randomized trials), inconsistent regulatory status across categories, and opaque pricing models that make ROI comparisons hard.

Business Models, Regulation, and Adoption Challenges

You’ll encounter subscription SaaS, per-case fees, outcome-based contracting, and partnerships with payers or providers. Startups like Viz.ai, IDx-DR (Digital Diagnostics) and Caption Health illustrate trade-offs: predictable recurring revenue versus per-screen reimbursement and the complexity of payer negotiations.

| Feature | Viz.ai | IDx-DR (Digital Diagnostics) | Caption Health |

|---|---|---|---|

| Business model | Enterprise SaaS + hospital licensing | Per-screen fees and SaaS to clinics; partnerships with health systems | Enterprise licensing and subscription to clinics and OEM partners |

| Regulatory status | Multiple FDA 510(k) clearances for stroke workflow | FDA-cleared autonomous AI for diabetic retinopathy screening (De Novo) | FDA-cleared AI guidance for cardiac/OB ultrasound acquisition |

| Pricing/reimbursement implications | Mostly hospital capital/operational budget; limited direct CPT codes; ROI via reduced time-to-treatment | Some CPT-level reimbursement is available for diabetic retinopathy screening workflows; often negotiated with payers | Reimbursement tied to billed ultrasound exams; AI guidance bundled under procedure codes |

| Integration & workflow | Requires PACS/EHR integration; workflow change management is significant | Designed for primary care workflows; EMR integration needed for referrals | EHR and device integration; training for sonographers/clinicians |

| Typical buyers | Hospitals, stroke centers, health systems | Primary care networks, health systems, payers | Health systems, imaging centers, primary care clinics |

Regulatory and reimbursement hurdles

FDA pathways differ by function: 510(k) clearances suit workflow augmentation, while De Novo or PMA may apply to autonomous diagnostics. You must budget for real-world performance monitoring, clinical validation, and compliance with HIPAA plus state privacy rules.

Integration and operational barriers

EHR and PACS integration costs, clinician workflow disruption, and vendor support determine adoption speed. Because few direct CPT codes exist for many AI services, you’ll likely rely on value-based contracting or internal cost-savings to justify ROI.

Provider vs Payer Approaches

Provider-focused SaaS (Viz.ai)

Enterprise workflow triage is sold to hospitals and stroke centers.

- • Enterprise licensing or seat-based subscription

- • FDA 510(k) clearances for stroke/triage tools

- • Integration with PACS and EHRs (Epic, Cerner)

Payer/Population Health Partnerships (IDx-DR)

Screening-as-a-service for payers and health systems.

- • Autonomous AI with FDA clearance

- • Per-screen reimbursement or negotiated value-based contracts

- • Designed for primary care/workflows, ties to preventive care metrics

- Assess pricing model vs likely reimbursement pathway.

- Budget for EHR/PACS integration and clinician training.

- Factor regulatory classification and post-market obligations into timelines.

Pros and Cons: A Balanced Review

🚀

Important Insight

Pilot admin automation; defer autonomous diagnostics until robust validation.

Pros

You’ll see clear upsides: improved diagnostic speed and consistency with PathAI and Viz.ai, operational efficiencies from Olive and Epic integrations, Atomwise and Recursion accelerating drug discovery, and personalization via Tempus and Butterfly Network imaging.

Heavy venture funding — exemplified by Sequoia-backed PathAI and SoftBank-backed Tempus — fuels rapid innovation but can compress clinical timelines.

Cons

Downsides are material: data bias and equity gaps, privacy and cybersecurity risks, opaque models lacking explainability, inconsistent clinical validation, and regulatory and reimbursement uncertainty.

Practical weigh-up

For low-risk use like administrative automation with Olive or Komodo Health pipelines, you should move from pilot to scale once ROI, audit trails, and vendor attestations are solid. High-risk scenarios — autonomous diagnostic decisions from PathAI or Viz.ai auto-triage — require prospective trials, third-party audits, and clear liability frameworks before scaling.

Recommendation

Evaluate trade-offs by matching clinical need, existing evidence, and resource readiness: prioritize validated endpoints, demand explainability reports, budget for monitoring, and stage pilots with vendor-neutral metrics before large deployments with clinicians.

Frequently Asked Questions

You’ll find targeted answers below addressing diagnostics, regulation, privacy, impact areas, vendor validation, and timelines. The quick FAQ highlights practical expectations when evaluating startups like PathAI, Viz.ai, Tempus, Olive, and Caption Health.

How do US startups use AI to improve diagnostics and clinical workflows?

▼

What regulatory hurdles do AI healthcare startups face when bringing products to the US markets?

▼

How are patient privacy and data security handled?

▼

Which clinical areas show the fastest meaningful impact?

▼

How should providers evaluate AI vendors and validate claims?

▼

What are realistic timelines and costs for piloting and scaling?

▼

Pros and Cons

- Pros: Faster reads and actionable flags from PathAI and Viz.ai, measurable ROI in radiology and RCM via Olive, stronger oncology datasets from Tempus.

- Cons: FDA clearance and post-market monitoring can delay deployment, high data-labeling and integration costs, and risk of model drift without robust monitoring.

Conclusion

As a reviewer of AI in Healthcare: How USA Startups are Leading, you’ll see US startups such as Tempus, PathAI, Viz.ai and Olive driving impactful adoption through venture funding, concentrated talent pools, and focused clinical use-cases. They convert research into deployable products that often outperform legacy workflows.

🎯 Key takeaways

- → US startups (e.g., Tempus, PathAI, Viz.ai, Olive) drive adoption via funding, talent, and focused clinical use-cases.

- → Balance innovation with rigorous validation: demand external trials, bias audits, and transparent performance metrics.

- → Next steps: run pilots with measurable endpoints, require transparent data, and plan EHR integration plus governance and clinician oversight.

Pros

- Rapid innovation cycles and VC-backed scale (Tempus, Olive).

- Strong clinician partnerships (Viz.ai stroke routing, PathAI diagnostics).

- Practical EHR integrations and deployment pilots.

Cons

- Variable external validation; many models lack prospective trials.

- Data bias risks when training sets aren’t representative.

- Integration costs and governance burdens for hospitals.

Next steps: prioritize pilots with measurable endpoints, demand transparent performance data, and plan for integration and governance with clinician oversight.

TL;DR: U.S. AI healthcare startups—exemplified by Tempus, Olive AI, PathAI, Insitro, and Viz.ai—are rapidly turning machine learning into diagnostic tools, workflow automation, and precision‑medicine platforms by leveraging talent hubs, venture capital, large clinical datasets, and pragmatic FDA pathways. This review summarizes funding and adoption trends, compares technologies and business models, and offers practical takeaways and trade‑offs for investors, clinicians, and product leaders.

In conclusion, the integration of AI in healthcare is not just a trend; it is a necessity for a more efficient and accurate medical future. USA startups are setting a gold standard that the rest of the world is now following. As we move deeper into 2026, staying updated with these advancements is crucial for healthcare professionals and tech enthusiasts alike. At SearchAIFinder, we are committed to bringing you the latest insights into these groundbreaking technologies. Which of these AI healthcare innovations do you think will have the biggest impact on our lives? Let us know in the comments below and join the conversation!

“Don’t miss the next medical revolution! 🩺 Join 5,000+ tech enthusiasts and get the latest AI insights,

startup news, and exclusive guides delivered straight to your inbox. It’s free!”

[📩 Subscribe to SearchAIFinder News]

I ‘m Md. Osman Goni > Founder of SearchAIFinder and an AI content specialist. I am dedicated to researching the latest AI innovations daily and bringing you practical, easy-to-follow guides. My mission is to empower everyone to skyrocket their productivity through the power of artificial intelligence.”

💬 We’d Love to Hear From You!

Which of these AI tools are you excited to try first? Let us know in the comments below!